Coronavirus / COVID-19 and Estate Planning

During the Coronavirus Pandemic, we are all connected by a shared concern for our families, businesses, and communities. We are anxious about our health and financial well-being. We are worried about being exposed and contracting the virus. What will happen if I get sick and become incapacitated? Or worse, what will happen if I die?

Essential Estate Planning Documents

Everyone should have these essential documents in place to protect them during incapacity, and to take care of their loved ones, if they die.

- Health Care Proxy authorizes your agent to make medical decisions for you, if you are incapacitated and cannot make the decisions for yourself.

- Durable Power of Attorney authorizes your attorney-in-fact to make financial decisions for you, including paying your bills and managing your investments and business.

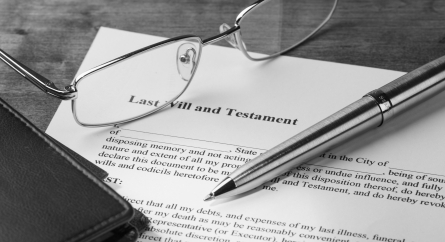

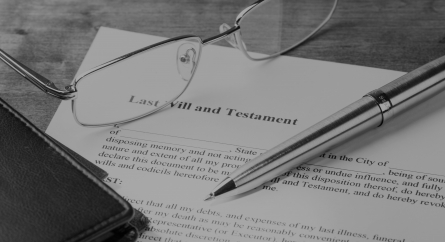

- Last Will and Testament designates a personal representative to gather your assets at your death, pay your debts and estate expenses, then distributes your remaining assets to your chosen loved ones. If you have minor children, you should appoint who you wish to serve as a guardian to care for them.

- Revocable Trust is a document for clients who wish to reduce their estate taxes and avoid the costs of the probate court. You can appoint a trustee to administer your assets on your behalf during incapacity, and to manage the assets for the benefit of your chosen loved ones upon your death.

- Beneficiary Designation Forms for your Retirement accounts and Life Insurance

You should review your beneficiary designations to ensure the persons named on the forms are who you wish to receive the assets at your death.

Leveraging a Down Market in Your Estate Plan

Some clients see a down market as an opportunity to leverage the asset value transfers to their loved ones, such as the following:

- Making Annual Gifts of the gift tax exemption amount ($15,000 per person in 2020) by gifting marketable securities, instead of gifting cash.

- Making Lifetime Gifts that utilize all or a portion of your lifetime estate tax exemption amount, by gifting marketable securities, real estate holdings, and business interests, instead of cash, to your loved ones or to an irrevocable trust, to be held for the benefit of your loved ones.

- Convert Traditional IRAs to Roth IRAs in a down market because the income tax on the conversion is calculated on the value of the marketable securities in the account. You will pay the tax during your lifetime, which reduces the taxes your loved ones will pay at your death.

Categorized: Estates

Tagged In: coronavirus, COVID-19, durable power of attorney, health care proxy, revocable trust, will