Qualified Small Businesses: When to Revisit the Structure of Business Operations

With the Tax Cuts and Jobs Act of 2017 corporate tax reduction, certain “qualified small businesses” should consider whether the corporate form provides them with more flexibility for future growth. Section 1202 of the Code exempts individual investors from tax on the gain from the sale of “qualified small business stock.” The gain exemption is limited to the greater of (a) $10 million or (b) 10 times the investor’s stock basis. The investor must hold stock in a C corporation for more than five years to qualify. At the time of the stock’s issuance and immediately after, the corporation must have assets with an adjusted basis of not more than $50 million (including cash). In addition, the corporation must be engaged in the active conduct of a qualified trade or business. Qualified trade or businesses encompass any active business except for: (a) professional service businesses (such as law, engineering, and architecture firms), (b) banks, insurance, financing, leasing, and investing companies, (c) farming businesses, (d) oil and gas producers, and (e) hotel and restaurant operators. For qualifying businesses that reinvest a portion of their profits, operating in corporate solution may be preferable now to operating as a pass-through entity such as an LLC. Below is an example of the contrast.

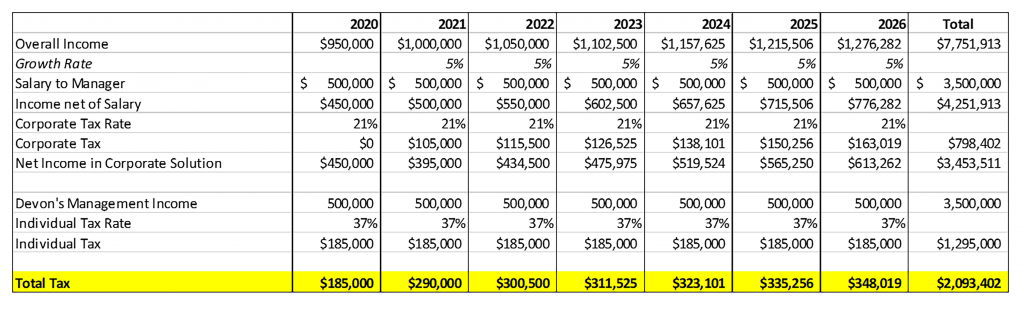

Devon runs a molding operation to manufacture complex medical devices and draws a salary for managing its operations. He has invested $15 million in the business. If Devon operates the business in corporate form (with the following assumed projections), below are the tax consequences:

If Devon operates the business in partnership form and takes a profit distribution but does not draw a salary, below are the tax consequences:

With the facts above, the effective tax rate operating as a corporation is lower than operating as a partnership for Devon’s business. In addition, if Devon holds onto the business for at least five years and subsequently sells it at a profit, gain of up to $150 million will be tax-free. Thus, the corporate solution provides Devon with more flexibility for future growth. This example shows it is time for business owners to revisit the structuring of their business operations.

Categorized: Taxes

Tagged In: Qualified Small Businesses, section 1202