Update Your Tax Withholdings to Avoid Year-End Surprises

During the 2022 tax filing season, many taxpayers had an unpleasant surprise when they filed their tax return and found out they were getting a much smaller refund than they were expecting, or worse, had a balance due.

Young people new to the full-time work force can be especially vulnerable to incorrect withholding, especially in the first complete year of full-time employment, since their income in prior years as part-time students was often offset by the generous standard deduction available to taxpayers. (For example, in 2021, single taxpayers received a standard deduction of $12,550, meaning if they earned less than that amount they owed no tax and any federal income tax withholding would be refunded.)

Frequently, unexpected surprises at tax time come from insufficient tax withholding.

Fortunately, it is not too late for taxpayers to adjust their 2022 tax withholding to avoid this result. The Internal Revenue Service website has a tool to assist taxpayers in determining the correct payroll tax withholding.

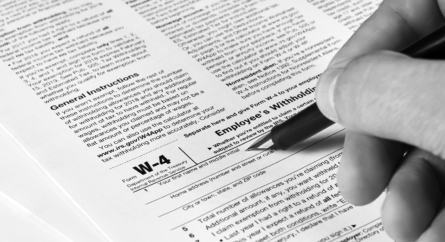

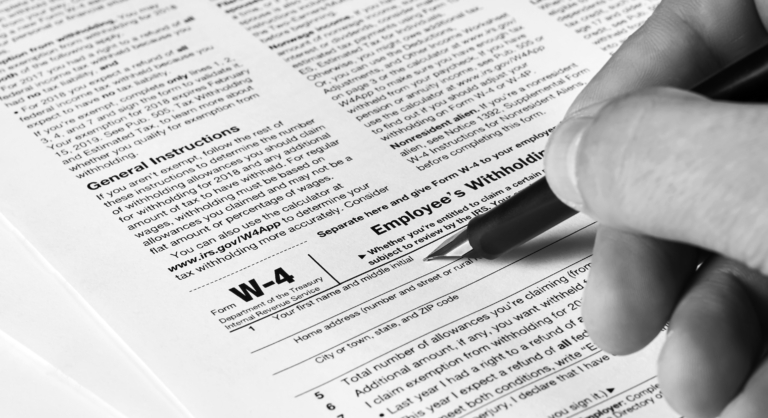

Armed with a recent pay stub and a copy of last year’s tax return, taxpayers can perform a payroll check-up and, if necessary, adjust their payroll tax withholding to avoid an unpleasant surprise in the spring. To change their federal tax withholding, taxpayers will want to complete a new W-4 and submit it to their payroll department.

In 2020, the W-4 was redesigned to closely align tax withholding with expected tax liability. However, if a taxpayer wants to make sure they receive a tax refund at tax filing time (many people rely on tax refunds as a form of forced savings), they should include an amount on line 4(c) for additional withholding per pay period.

For example, a recent college graduate was disappointed to learn in February 2021 that an expected $2,000 refund was actually a $60 refund. The new graduate decided she would have an additional $40 per bi-weekly pay period withheld by completing a new W-4 and including $40 on line 4(c). If she has no other income, she should expect a refund in the $1,000 range when she files next year (26 pay periods x $40 =$1,040).

Categorized: Taxes

Tagged In: IRS, payroll tax withholding, tax returns, W-4